China's regulatory crackdown

While the Chinese Communist Party (CCP) has been celebrating its 100th anniversary, focusing its long-term strategy on growth with equity for the benefit of all and looking to boost its birth rate in the face of an ageing population, we are seeing a regulatory tsunami.

Alongside China’s regulators, their European and US counterparts (Ms Vestager, I’m looking at you…) are pale imitations. The violence and speed of regulatory change in China is par for the course in a country where everything happens faster.

Although it is difficult to pinpoint when this wave of regulation began, we can nonetheless pick out 3 November 2020 as a pivotal moment. ANT FINANCIAL GROUP1, the financial arm of ALIBABA, was about to launch the biggest IPO in history, raising more than $37 billion (only slightly short of the GDP of Bolivia…). This IPO was such an event, it was oversubscribed to the tune of $2.8 trillion – about the size of UK GDP!

However, Jack Ma had become something of a celebrity, being treated by the highest international authorities as a spokesman for China, and his scathing comments on the Chinese banking sector – especially the state-owned banks – being slow to adapt and falling short on innovation, unleashed the fury of the CCP. The IPO of ANT FINANCIAL GROUP was cancelled, and Jack Ma disappeared for three months, when people began to fear the worst for the Chinese billionaire. Mr Ma has kept a low profile ever since.

In our eyes, this attack, which seemed to target Jack Ma and his celebrity status, quickly became a demonstration of the CCP flexing its muscles, as it sought to show who was in charge of the country. On the other hand, this was not the first time that the CCP had taken

aim at the tech sector. Back in 2017, amid the unstoppable rise of China’s internet giants BAIDU, ALIBABA and TENCENT, the CCP wanted to acquire a 1% stake in these companies along with a seat on their boards, so it could have its say on their strategic decisions. This was becoming even more urgent, as the companies rapidly grew much bigger than state-owned firms. What if the CCP was losing its grip on the main driver of China’s economy?

Very quickly, in the wake of the cancelled ANT GROUP IPO, the regulators swooped on ALIBABA’s anti-competitive practices, which obliged sellers on its e-commerce platform to sign exclusive agreements, preventing them from selling their products on other platforms. This made potential competitors less attractive if they were unable to offer the most interesting or popular products. For a long time, this situation prevented other marketplaces emerging that could compete with ALIBABA. But with PINDUODUO bursting onto the scene, the battle lines were redrawn, and the company’s recent shift in strategy is particularly interesting in the context of the uncertain regulatory environment. The Chinese regulators eventually decided to issue a record fine of $2.8 billion and prohibit e-commerce companies from offering exclusivity agreements (among other restrictions).

PINDUODUO provides an interesting example. At lightning speed, it became the world’s second-biggest company after Google to reach a market cap of $100 billion following its IPO (source: Acquired), and even overtook ALIBABA at the start of the year in terms of annual active client numbers.

The company co-founded by Colin Huang, who had met the legendary investor Warren Buffett over a dinner won in a charity auction, also risked being in the regulator’s sights, and needed to take action.

First of all, Colin Huang stepped down from his position as CEO, and a few months later, resigned as Chairman, leaving a management team and new board to pick up the reins.

Having avoided the celebrity route chosen by Jack Ma, Colin Huang said he wanted to concentrate on new opportunities that would allow companies with a positive impact on China’s economy and society to emerge.

Next, PINDUODUO focused on its ability to give Chinese farmers an online presence and enable them to increase their sales and reduce waste, as well as helping Chinese citizens to become farmers. Beyond the benefits of improving the standard of living of farmers through technology and providing greater access to customers via the internet, the company was protecting itself from feeling the full force of the regulatory crackdown. To understand how important this strategy was for the company, take a look at its investor relations page.

The omniscient eye of the CCP quickly turned to another sector that was not falling into line with the Party’s centenary goals: education. In a country of more than 1 billion inhabitants, access to China’s best universities is the favoured route to breaking glass ceilings. But given the large number of inhabitants and small number of top universities, competition for places has risen to extreme levels. While a heavy schedule of study is pretty common in Asia, China tops the table by some distance. In Japan, South Korea and China, it is not uncommon for even very young children to study from 8am to 8pm, or even longer. In China, this has meant private tutoring developing into a gigantic, dynamic and profitable market. The tutoring companies have rapidly become impressive stock market performers, as well as a ‘must have’ for emerging and global investors. Having grown to a value of more than $100 billion before the regulatory clampdown, this sector has suddenly been cut down in its prime. China announced earlier this year that couples would be permitted to have up to three children, in a further departure from the one-child policy. With the inevitable demographic decline caused by this policy, and faced with China’s ageing population, boosting the birth rate has become a priority. This is why regulating the price of education has become such an issue, and taking greater control of the sector also enables the government to oversee the content being taught. Lowering tutoring costs and controlling content are the two main objectives of the new regulations. The reforms are drastic: tutoring companies must become non-profit

entities. They will no longer be able to raise capital abroad, and tutoring outside school hours, at weekends and during holidays will be limited. Unsurprisingly, the biggest sector players plummeted by more than 90% in a few days – a record.

What is the current situation, and how will it play out?

The situation is evolving very rapidly. DIDI, China’s UBER, went ahead with its IPO despite the regulatory risks, but investors have paid a high price, with the stock losing half of its value since the flotation. A massive sell-off of Chinese securities across the board is under way, but with tech and healthcare stocks particularly impacted as investors fear the worst for these sectors. This is slightly reminiscent of the collapse of Lehman Brothers, which signalled to the world that the worst could happen. Given the unpredictability of the CCP, this tide of panic is especially difficult to analyse. You could even go as far as to suspect that the party is engineering an exodus of foreign investors, who are suffering immense losses, so as to enable local investors to pick up these high-quality assets at bargain prices. China has a very clear ambition: to become the world leader in tech and displace the US as the biggest global economy. These goals feature in the CCP’s five-year plans. It therefore seems unlikely that this is the end of the story for innovative sectors such as tech and healthcare, since in the long-term, they will be China’s main value creators (jobs, tax revenue, better quality of life). But in the short term, anything is possible.

It looks to us as if the current wave of regulation is particularly affecting sectors in which the established giants have become quasi-monopolies. Given China’s aim of fostering innovation and enabling a new generation of players to emerge and become world leaders in new technologies such as robotics, artificial intelligence, 5G and gene editing, and in the space sector, we think these companies will come to benefit from a more even playing field.

As for the possibility of investing in Chinese assets, it is unlikely that China will go back on its plan to relax rules on foreign investment. However, the country may want to impose stricter regulation on the existing VIE (variable interest entity) structure, which enables foreign investors to gain an economic interest in Chinese assets through indirect investment agreements. We could see changes to this grey area, for example with companies having to obtain a listing in mainland China via A-shares, effectively forcing investors in VIEs to shift into A-shares, whereby capital inflows and outflows are controlled via the Hong Kong Stock

Connect system. It therefore remains to be seen whether emerging and global investors will be able or keen to take this path.

Lastly, we think that decisions carry the most importance when uncertainty is at its highest. Crashes are often perceived as an opportunity, once the storm has passed, but when we are in their midst, they are more likely seen as a risk. Our strong conviction on China is for the long term, and is based on its innovation capability, its rapid adoption of new technologies and new ways of living, and its structural advantages, such as its huge population. A black swan event could still happen, but it is not our core scenario. We are navigating these choppy waters with enthusiasm, but these unprecedented times also require caution.

How are these events impacting Echiquier Artificial Intelligence and Echiquier World Next Leaders?2

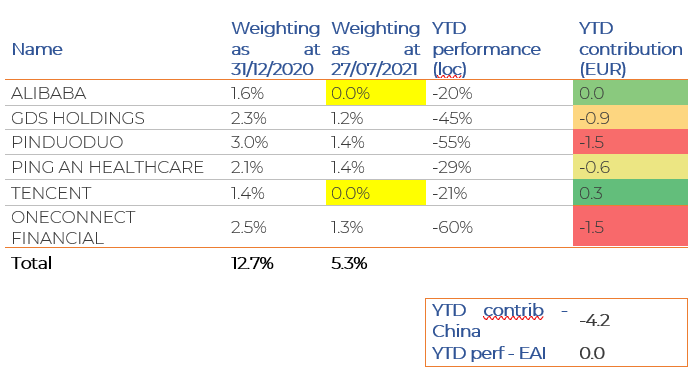

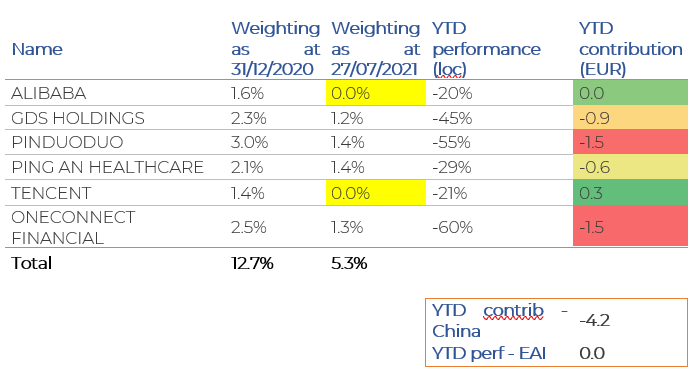

For Echiquier Artificial Intelligence, the impact is significant, but limited by the weighting of Chinese stocks in the portfolio. At the start of 2021, 10% of the fund was invested in Chinese companies. These companies have experienced major drawdowns in recent weeks, as well as periods of growth/value rotation between February and May. Over the year, we decided to sell off TENCENT for valuation reasons, followed by ALIBABA, on regulatory fears over its leading position in the e-commerce, cloud and payments sectors. So far this year, these two stocks have made a neutral/positive contribution to the fund’s performance.

However, the other stocks in the portfolio have been significant detractors (-4 percentage points), although the fund’s performance has been flat year-to-date.

The business models of the companies still in the portfolio are very robust in our opinion and consistent with the CCP’s goals. For example, PING AN HEALTHCARE & TECHNOLOGY is helping to reduce hospital congestion by facilitating access to a doctor at prices any Chinese citizen can afford. ONECONNECT FINANCIALS, meanwhile, offers banks and other financial institutions in China access to digitalisation modules to make them more competitive vis-à-vis new entrants, as well as enabling them to provide users with a better service and lowering their costs. As mentioned above, PINDUODUO is playing an increasingly active role with agricultural producers and is well placed to upsell its platform to capture an ever greater share of China’s e-commerce market. This will make the market more competitive, while also protecting sensitive activities such as agriculture. We do not see this company being affected by regulatory risk. Lastly, the immense data centres of GDS HOLDINGS are helping to digitise the Chinese economy. Historically, the government has supported the group, but we fear that it will prefer to favour smaller players to stop the sector from becoming a quasi-monopoly. This will affect market consolidation, a possible route to growth for GDS. We are keeping a close eye on this situation and think that GDS will find other ways to grow in Asia, as suggested by its recent expansion in Malaysia.

In the case of Echiquier World Next Leaders, at the start of 2021 it had a higher weighting of Chinese stocks than Echiquier Artificial Intelligence, at 21%. The weighting currently stands at around 19%, after a number of positions were strengthened in recent days. Year to date, the overall impact of the China component is -5 percentage points, which explains two-thirds of the fund’s decline so far in 2021, after a stellar rise in 2020. Despite the fall in 2021, it is worth remembering that the fund has delivered excellent long-term performances, gaining 120% over 3 years and 172% over 5 years.

Among stocks leaving the portfolio, we had already sold off our position in TENCENT MUSIC ENTERTAINMENT well before the regulatory wave, taking profits once our target price had been reached. We also sold YIHAI after it had posted strong gains, following a disappointing results release that reduced our confidence in the stock.

In terms of additions to the portfolio, we have initiated a position in AGORA, which we had been monitoring since its IPO. Its share price shot up initially before falling back sharply, when we took the opportunity to invest. Unfortunately, its decline has continued as regulatory risks weigh on the tech and education sectors. AGORA generates 15% of its revenue from tutoring companies that use its real-time video solutions for online classes. But despite the sector reforms, tutoring should continue in China. Abolishing it was never the aim, and the big advantage of online solutions is that they make education more accessible, especially for those who are unable to travel to tutoring centres. Nonetheless, AGORA may see its growth stall in this segment or be forced to lower its prices, which would impact this revenue stream but not remove it entirely. The company will likely look to expand via other segments, building on its international success with leading apps such as CLUBHOUSE and SPOTIFY, which use this technology.

As for WUXI BIOLOGICS, healthcare regulation is a concern for the market, but we see the company as one of China’s leading drivers of innovation in drug manufacturing. Moreover, it plays a major role in medicine research and production for large international pharma and biotech groups, making it a strategic stock in geopolitical terms. As such we think it will be less exposed to specific reforms.

Another Chinese stock in the portfolio is WUXI LEAD, which specialises in equipment for the manufacture of rechargeable batteries. The company is an enabler in the transition to electric vehicles, which is a major issue for China as the country wants to reduce its carbon emissions and be the global leader in energy transformation. Having risen since the start of the year, the stock should be protected from both current and future waves of regulation.

Lastly, we think KINGSOFT CLOUD looks well placed to prosper in the current environment. It is a more modest cloud player than the tech behemoths ALIBABA and TENCENT, and offers a third way to customers seeking an option outside these internet giants. The company prides itself on its ‘neutrality’ vis-à-vis its customers and will take on any type of cloud project. Its presence has made China’s cloud market, which is still in its infancy, more dynamic and has broken the ALICLOUD/TENCENT CLOUD duopoly. By stimulating competition and enabling market share to be spread more evenly, it seems to be aligned with the regulator’s objectives.

Our long-term conviction on China remains strong, thanks to its innovation capability, its rapid adoption of new technologies and new ways of living, and its structural advantages, such as its huge population. We could still see a black swan event, but this is not our core scenario. We are navigating these choppy waters with enthusiasm, but these unprecedented times also require caution.

Rolando Grandi, CFA3

Drafted on 28/07/2021

1 All stocks referred to are given by way of example.

2 The positions shown are as at 27 July 2021. This data may change over time.

3 The views expressed herein are those of the fund manager as at the date on which this article was written, and may change over time.