Convertible bonds: an especially favourable backdrop

The convertible bond is a bond with a twist: the right to convert into shares of the issuing company, making it a hybrid instrument that is highly adaptable to varied market environments, useful in turbulent equity markets.

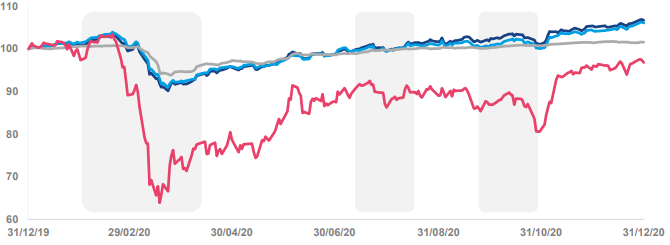

Convertible bonds in 2020 : in a class of their own !

By nature, a convertible bond is characterised by its convexity: its ability to capture bullish equity markets and cushion its downturns.

In many ways, 2020 was a year of firsts, but one thing remains constant: the convexity of convertible bonds has been a real advantage.

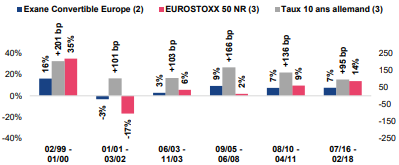

Comparative Performance1 31/12/2019-31/12/2020

● Illustration of the convexity of convertible bonds ●

How do we explain the resilience of European convertible bonds ?

The quality of the pool | From the start of 2020, the European convertible bond pool showed good credit quality: a distance to the floor of around 11%, and 62% of the field was rated “Investment Grade”2. Remember that even when the markets drop, the bond floor does even better as a shock absorber if the issuers’ intrinsic credit quality is good.

The convexity of the pool | The convexity of the pool at the start of 2020 also contributed to the solid performance of the asset class: at the time, nearly 50% of the pool had a so-called “mixed” profile (i.e. equity sensitivity of 30%-70%), and average equity sensitivity was 32%2. All other things being equal, the pool was ideally positioned to take on a turbulent year.

A buoyant primary market | In addition, 2020 has seen many issues of European convertible bonds on the primary market: 46 issues in total for more than €23 billion2. This amount has been steadily increasing since 2017, and the universe of European convertibles is benefiting from its momentum: diversifying in terms of issuer sizes, sectors, risk profiles, etc.

The proliferation of issuers and their profile has restarted and stabilised flows in the asset class: diversification is good for the pool, its quality, and its fundamentals. As such, our analysis shows that 2021 is starting with positive parameters and promising prospects.

Past performances are not a reliable indicator of future performances and may vary over time. Data as of 31/12/2020.

Sources : La Financière de l’Echiquier, Bloomberg1, Exane Derivatives2.

European convertible bonds in 2021 : is this the right time ?

Attractive discounts | When equity and credit market valuations look relatively demanding, convertibles have an attractive discount, below its past five-year average; our analysis even shows that it is at one of its lowest points since 2011. Combined with the pool’s good credit quality, convertibles seem like an appealing investment alternative to continue to capture equity and credit market upside, while at the same time profiting from a decelerating effect in the event of a downturn. It should also be noted that listed options’ volatility is almost back at pre-crisis levels: convertible funds can then seek this additional convexity using options in addition to convertible bonds.

Europe has the lead ! | In Convertibles – Europe vs. US, Europe seems to have the lead. First in terms of valuation: the European pool is cheaper. It has 2.5 times more discounted convertibles than overpriced convertibles, while in the US field, those numbers are even1. In addition, the European delta is more attractive (49% vs. 76% in the US)1, with a very pronounced sector bias in the US, which accounts for a majority of Nasdaq issuers.

European Convertibles started off in 2021 with good quality, the resilience it demonstrated in 2020, and a steady stream of primary issues2: by annualising the first two months of 2021, we’re back to the pace of 2020, which meant diversification, refocusing in a “mixed” zone, and improved fundamentals.

And what if interest rates rise ? | The asset class has already shown its resistance to rate increases in the past. In fact, for a maturity similar to traditional bonds, it generally has lower sensitivity to interest rates. This is due in particular to the conversion option, which is likely to see its value increase, thus offsetting the impact of rate increases on the convertible’s bond component.

In addition, the pool of convertibles has been undergoing a profound “green” transition for several months, which we believe is promising.

Sustainability : a new performance catalyst for the pool ?

Convertibles in shades of GREEN | In 2019, La Financière de l’Echiquier (LFDE) published a study showing a positive correlation between Socially Responsible Investment (SRI) and equity market performance. And 2020 marked a real “green” turning point for convertible bonds. Let’s not forget that in 2020 we saw the first five issues of “green” convertible bonds in Europe accounting for 15% of the total amount of issues over the year, and the first issue indexed to sustainability3.

What does SRI management bring to the convertible bond universe ? Long-term outperformance of portfolios made up of stocks with the best ESG ratings; maximised risk/return ratio; resilience of companies with the best ESG profiles, in the event of market downturns; and more. According to our analysis, these contributions come from (i) their quality and the soundness of their balance sheet; (ii) clear identification and management of non-financial risks, particularly vital in a bear market; and, lastly, (iii) increasing inflows to these stocks, supporting their share price.

Certain convertible bond funds can use options, and have all the more opportunities if they use SRI management: they can position themselves on responsible stocks that are not necessarily convertible bond issuers.

Now, amid volatile markets and uncertainties about rates and growth, portfolio diversification and risk management must remain priority objectives. Convertible bonds are naturally hybrid and capture part of the potential rise in equity markets while limiting the risk of capital loss. This convexity, demonstrated by how the asset class fared, especially in 2020, and the improved quality of the pool, have persuaded us that convertible bonds have their place in an allocation.

Past performances are not a reliable indicator of future performances and may vary over time. Data as of 31/12/2020.

Sources : La Financière de l’Echiquier, Nomura1, Exane Derivatives2, Bloomberg3.

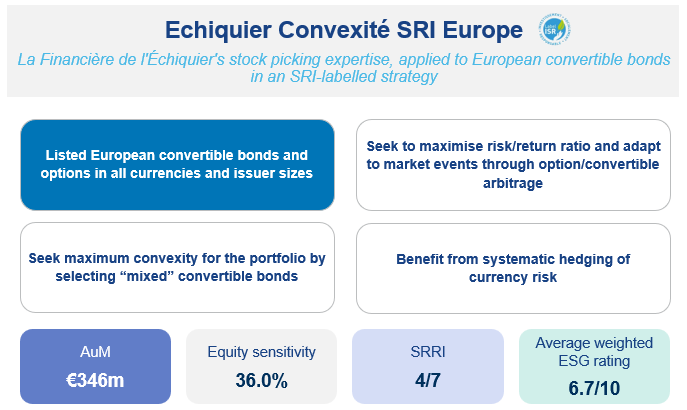

Echiquier Convexité SRI Europe : LFDE’s Convertible Fund

At La Financière de l’Échiquier in 2021, convertible bonds are managed through the Echiquier Convexité SRI Europe fund, which earned its SRI label in December 2020. The management team has further developed its management process and its convexity-focused approach by incorporating sector exclusions to focus its analysis on the most virtuous securities in the pool, ESG filters, and requirements for the fund’s non-financial profile (including the fund’s carbon footprint and its commitment to portfolio companies).

Since the fund can use listed options and invest in European convertible bonds in all currencies, from any size issuer, in a pool that fully displayed its convexity in 2019-2020, it seems well positioned to use the advantages of the hybrid nature of convertibles: capturing the upside of a bull equity market and cushioning the impact of a bear market.

Echiquier Convexité SRI Europe A : FR0010377143 | Benchmark : Exane Convertible Europe Hedged

Echiquier Convexité SRI Europe I : FR0010383448 |Recommended investment period: 3 years