Momentum - Value investing in Europe : poised for a rally?

As US entrepreneur and investor Robert Arnott said, when it comes to investing, “what is comfortable is rarely profitable”. The first half of 2018 may have been dominated by growth stocks in terms of

performance, but the outlook is now looking better for value investing.

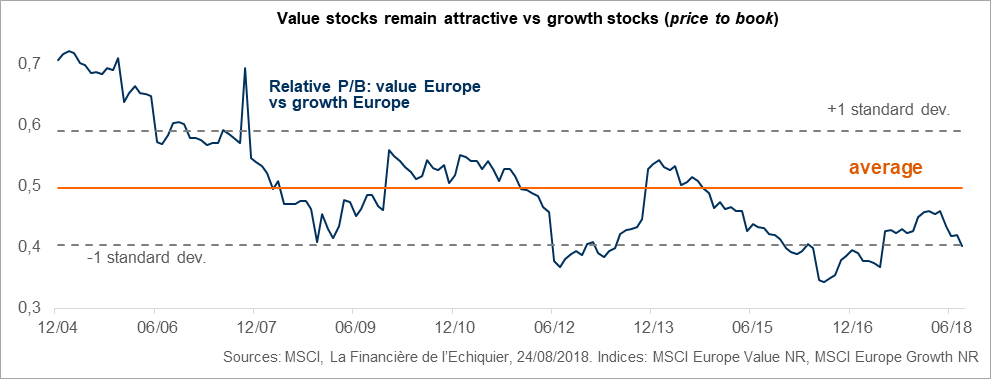

Value investing, a strategy that relies on picking stocks which are undervalued by the market, hit a low point in terms of relative value (at 31/08/2018 the MSCI EMU Value index stood at -3.9% YTD

compared to +6.3% for the MSCI EMU Growth). Uncertain politics in Europe coupled with fears stoked by the threat of a trade war fostered a wait-and-see approach and inhibited risk-taking, while the wobble in European growth killed off the bullish mood that had swept markets in 2017. With ECB quantitative easing also having helped keep interest rates at historic lows, investors temporarily turned away from discounted stocks and favoured growth stocks which they considered less risky.

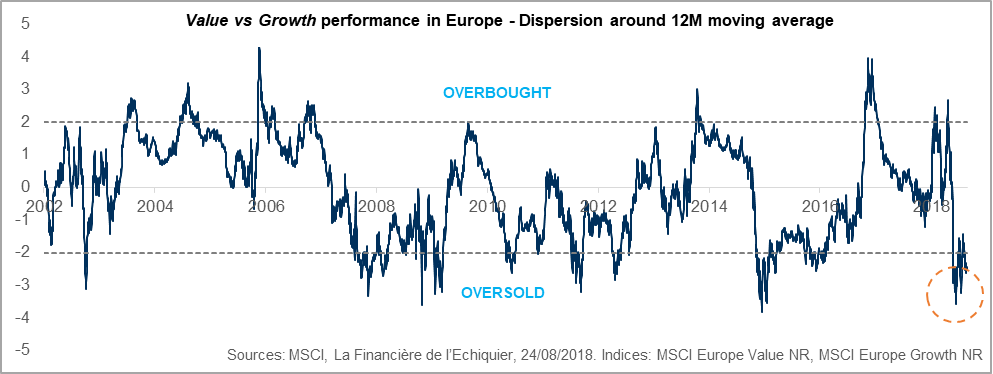

Value stocks in Europe are now in oversold territory, with discounts back to levels last seen in the immediate aftermath of the Brexit vote or the heat of the 2011 sovereign debt crisis. At the depth of

the market fall-back in June, the relative performance of value vs. growth in Europe was over 4 standard deviations below its 12-month moving average. We can now look toward the rebound, such

levels having historically represented good entry points for undervalued stocks.

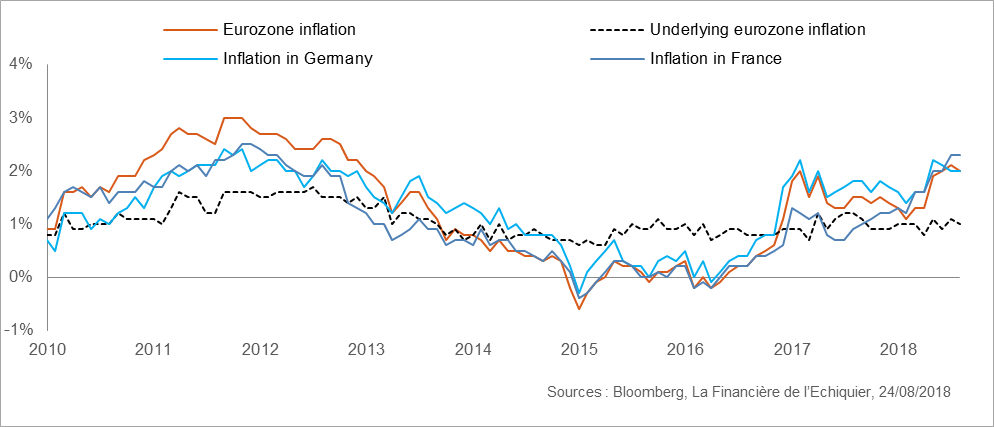

The economic environment also looks promising. The ECB has announced the end of overly accommodative monetary policy, holding out the prospect of normalised interest rates. This, coupled

with accelerating inflation in the eurozone, should be good for value investing.

Rising bond yields and inflationary expectations have historically been strong performance drivers for the strategy. Value stocks are often cyclical and tend to deliver good performances when the

economy recovers. This is particularly true of banks, industrial stocks and the energy sector which can look forward to commodity prices increasing on the back of rising demand from a quickening economy.

We have seen a gradual drift in indicators towards more bullish territory: European unemployment is declining and households remain confident. After the wobble early in the year, the return to healthier fundamentals and the rebuilding of upside for European stocks have created favourable market conditions for the strategy.

We remain confident that European markets will prove resilient : the value theme has suffered from the emergence of new risks but this is not the time to abdicate!