2019: are convertible bonds making a comeback?

An asset class with a real edge

The convertible bond is a classic bond with a twist: the right to convert into shares of the issuing company, making it a hybrid instrument that is highly adaptable to varied market environments, and particularly useful in turbulent equity markets.

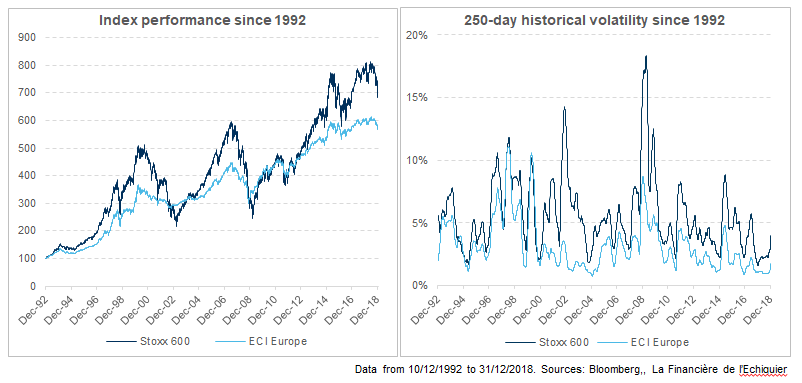

There is a lot to like about convertible bonds. Their long-term performance is comparable to that of equities (annualised performance of the Exane ECI Europe TR was +3.95% over the last 20 years, against +3.61% for the Stoxx Europe 600 NR) with between half and a third the volatility (annual volatilities of respectively 7.7% and 18.5% for the same indices over this period). The protection offered by bonds – redemption price is known in advance – also means that investors can capture some of the upside of equity markets but suffer a smaller part of the downside.

Finally, convertible bonds have historically done well in times of rising rates (due to short duration relative to other fixed-income assets, and optionality). This makes them an attractive play in the context of monetary policy normalisation.

Major indices ended January with positive performances. But 2019 is shaping up to be a year of volatile markets. Political instability and monetary tightening in the US are clouding visibility for investors and, with eurozone sovereign debt paying historically low yields, finding new sources of yield has become essential. This environment seems particularly suitable for convertible bond investing, especially since the asset class is currently looking very attractive.

An attractive market for convertibles

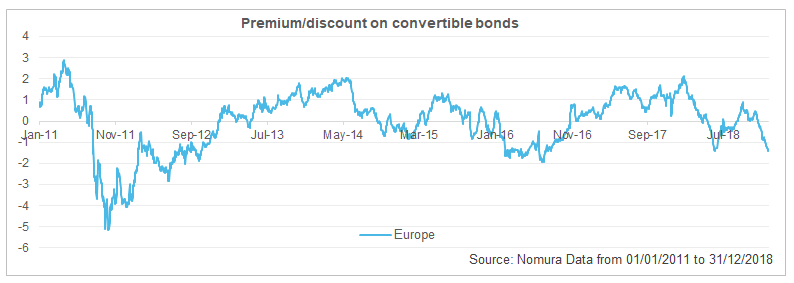

Trading at discounts

2018 ended six years of unbroken gains for convertible bonds. The recent dip largely reflects underperformances of blue chip convertible underlyings against equity indices (-18% vs. -14% for the Euro STOXX 50) and mid-cap underlyings (-26.3% vs. -15.9% pour le MSCI Europe SMID), as well as a sharp widening of credit spreads on investment grade and high yield. The European pool of convertible bonds is currently trading at a marked discount and has therefore rebuilt its upside for 2019.

Convexity looking attractive again

Nearly 50% of European convertible bonds in issue are now well placed in the “mixed” zone, with an equity sensitivity between 20% and 80%, a profile that can maximise the appeal of the asset class (higher upside on market rises but a floor to cushion the falls).

Positive yields are back

We are seeing many convertibles return to positive or zero yield: this applies to over 60% of issues compared to just 48% a year ago.

Improved credit quality

Credit quality in the convertibles universe has shown a sharp improvement. More than 70% of issuers are now rated investment grade vs. 45% at 31/12/2017. Credit quality also reflects a healthy sector diversification in the pool, unlike the US, for instance, where risky sectors like techs and biotechs are overrepresented.

More liquid pool of instruments

More than 50% of convertible bonds have issue volumes above €500M, compared to less than 40% at end-2017, which means the European bond pool now offers better liquidity.

The market fall has narrowed the distance to bond floor and restored an attractive convexity at historically low prices.

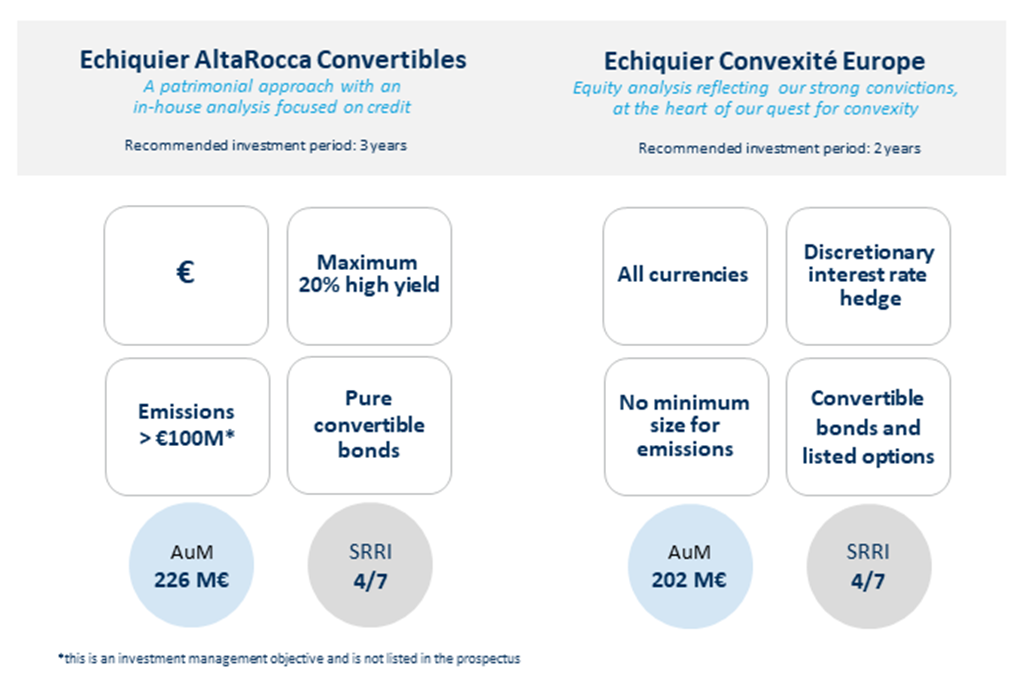

2 mutual funds, 2 investment profiles for this asset class

At La Financière de l’Echiquier, we manage convertible bonds via two complementary strategies. Echiquier AltaRocca Convertibles has adopted an investment approach based on in-depth credit analysis within the asset class. Echiquier Convexité Europe adopts a more equities-sensitive approach, centred on convexity research.

At this time of market volatility, portfolio diversification must remain a key objective. Convertible bonds are a hybrid instrument by nature and capture part of the rise in equity markets while limiting the risk of capital loss.

Echiquier AltaRocca Convertibles A: FR0011672799

Echiquier AltaRocca Convertibles I: FR0011672807

Echiquier Convexité Europe A: FR0010377143

Echiquier Convexité Europe I: FR0010383448